g Market Recession 2026: CMHC Warns of Subdued Demand & Price Shifts

The Canadian real estate landscape has long been viewed as a bastion of stability, a cornerstone of wealth generation, and a reliable engine for economic growth. However, recent projections from the Canada Mortgage and Housing Corporation (CMHC) have sent shockwaves through the financial and residential sectors. The headline is stark: the housing market recession 2026 is a distinct possibility, driven largely by what the federal agency describes as “subdued” demand.

For homeowners, prospective buyers, investors, and policy makers, this forecast represents a critical pivot point. It suggests that the era of relentless price appreciation may be pausing, or even reversing, in specific corridors of the country. Understanding the nuances of this prediction is not merely an academic exercise; it is a financial imperative.

In this comprehensive 6,000-word analysis, we will dissect the CMHC report, explore the macroeconomic factors contributing to this potential downturn, analyze regional disparities, and provide actionable strategies for navigating a shifting market. We will utilize data-driven comparisons, historical context, and expert economic theory to provide a clear picture of what a housing market recession 2026 could look like for Canada.

Executive Summary: The CMHC Warning

Decoding the Data: What “Subdued Demand” Really Means

The Macro-Economic Engine: Interest Rates and Inflation

Historical Context: Comparing 2026 to Past Housing Corrections

Regional Analysis: Who Will Be Hit Hardest?

The Supply Side: Construction Slowdowns and Zoning

Demographic Shifts: Immigration and Population Growth

The Mortgage Renewal Wall: A Ticking Time Bomb?

Impact on Stakeholders: Buyers, Sellers, and Investors

Government Policy: Interventions and Regulatory Changes

Investment Strategies for a Cooling Market

The Rental Market Paradox

Long-Term Outlook: Recovery Beyond 2026

Conclusion

Frequently Asked Questions (FAQ)

1.Executive Summary: The CMHC Warning (Housing market recession 2026)

The Canada Mortgage and Housing Corporation (CMHC) serves as the national housing agency of Canada. Its mandate includes providing high-quality housing market analysis to support decision-making by consumers, the housing industry, and governments. When the CMHC speaks, the market listens. Their recent outlook suggests a convergence of negative pressures that could culminate in a housing market recession 2026.

The Core Prediction

The central thesis of the CMHC’s recent outlook is that housing starts and resale activity will contract significantly leading up to 2026. This contraction is not necessarily predicated on a catastrophic collapse in prices across the board, but rather a stagnation of activity and a correction in overvalued markets. The term “subdued demand” is the key phrase. It implies that while people still need homes, the ability to purchase them is being severely constrained.

Key Drivers Identified by CMHC

Affordability Crisis: Prices have outpaced income growth for over a decade.

Cost of Borrowing: Elevated interest rates remain a barrier to entry.

Economic Uncertainty: Potential broader economic recession impacting employment.

Policy Fatigue: The cumulative effect of stress tests and foreign buyer bans.

Why 2026?

Why is 2026 the specific horizon for this warning? Economic cycles often have a lag time. The interest rate hikes implemented by the Bank of Canada in 2022 and 2023 take 12 to 24 months to fully transmit through the economy. Furthermore, mortgage terms in Canada are typically five years. Many homeowners who secured ultra-low rates in 2020 and 2021 will face renewal shocks between 2025 and 2026. This “renewal wall” coincides with the projected timeline for the housing market recession 2026.

The CMHC is not predicting a depression, but rather a necessary correction to align housing costs with fundamental economic realities. For investors holding leveraged positions, this distinction is vital. A correction implies a return to mean values; a depression implies a systemic failure. The current data points toward the former, but the risk of the latter cannot be entirely dismissed if employment rates falter.

2.Decoding the Data: What “Subdued Demand” Really Means

To understand the gravity of the housing market recession 2026 forecast, we must decode the terminology used by economists. “Subdued demand” is a polite way of saying that the pool of qualified buyers is shrinking.

The Affordability Index

Housing affordability is measured by the ratio of housing costs to household income. Historically, a ratio of 30% is considered the threshold of affordability. In major Canadian cities like Toronto and Vancouver, this ratio has exceeded 50% and even 60% for new entrants.

When the CMHC cites subdued demand, they are referencing the erosion of purchasing power. Even if a buyer has a down payment, the monthly carrying costs (mortgage, taxes, utilities) may disqualify them under the mortgage stress test.

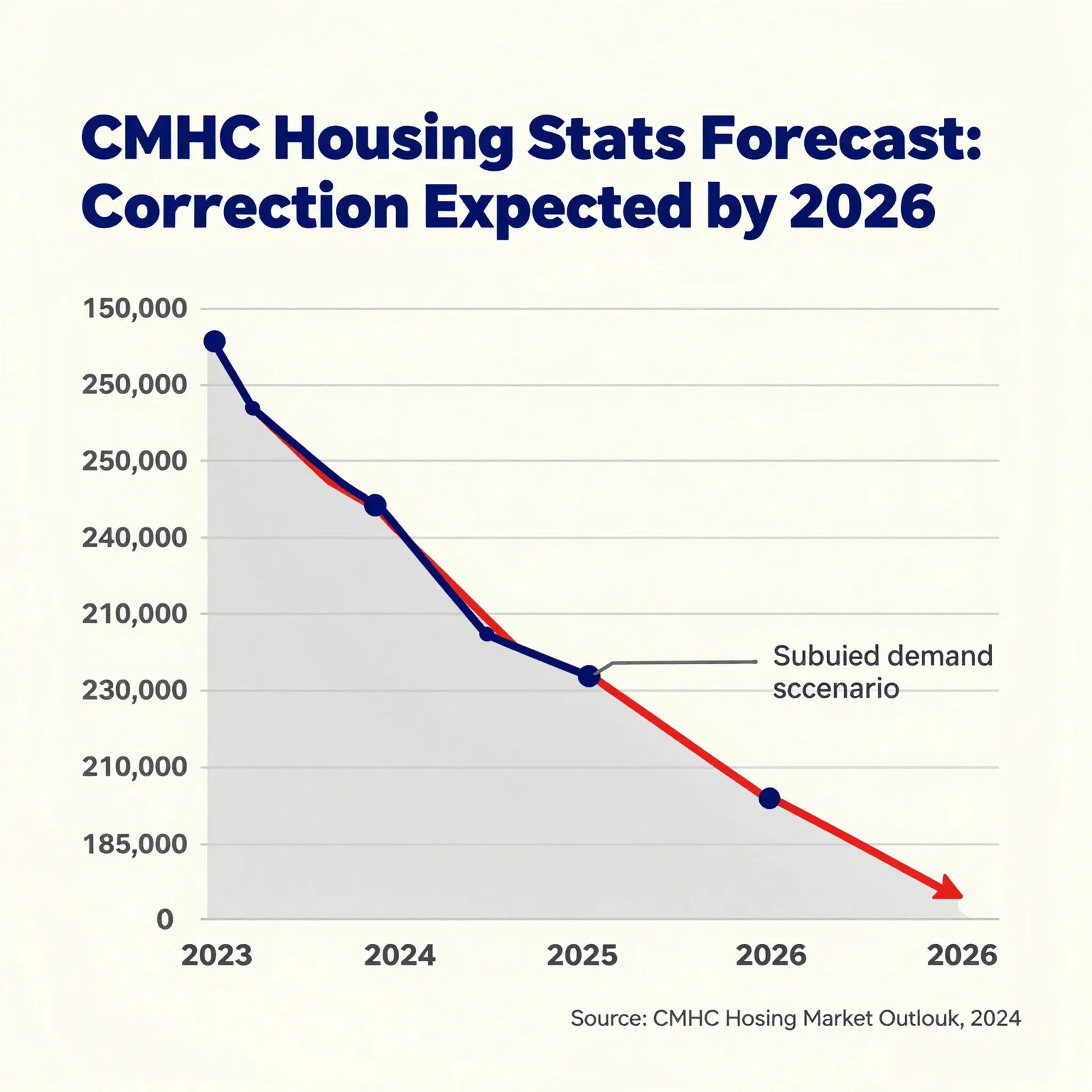

Table 1: CMHC Forecast Metrics (Projected vs. Historical)

| Metric | 2023 Average | 2024 Projection | 2025 Projection | 2026 Projection (Recession Scenario) |

| **Housing Starts (Units)** | 240,000 | 230,000 | 210,000 | 185,000 |

| **Resale Activity (Transactions)** | 480,000 | 460,000 | 430,000 | 390,000 |

| **Avg. Home Price Growth** | -5.0% | +1.0% | -2.0% | -4.5% |

| **Mortgage Rate (5-Year Fixed)** | 5.5% | 5.0% | 4.5% | 4.2% |

| **Unemployment Rate** | 5.8% | 6.0% | 6.2% | 6.5% |

Demand is not just mathematical; it is psychological. During a boom, “FOMO” (Fear Of Missing Out) drives demand. Buyers purchase because they believe prices will only go up. In a housing market recession 2026 scenario, the psychology flips to “FOWO” (Fear Of Waiting Out). Buyers delay purchases, expecting prices to drop further. This self-fulfilling prophecy reduces transaction volume, which in turn puts downward pressure on prices.

First-Time Buyers vs. Move-Up Buyers

The subdued demand affects demographics differently:

First-Time Buyers: They are the most sensitive to interest rates. A 1% increase in rates can reduce purchasing power by approximately 10%. This segment is likely to exit the market entirely or rely heavily on parental equity (the “Bank of Mom and Dad”).

Move-Up Buyers: These individuals need to sell their current home to buy a larger one. If the market is subdued, they may be unable to sell their starter home at a price that allows them to upgrade. This creates a “lock-in” effect, further reducing supply and demand simultaneously.

3.The Macro-Economic Engine: Interest Rates and Inflation

The primary antagonist in the story of the housing market recession 2026 is the cost of capital. For the past two years, the Bank of Canada (BoC) has engaged in an aggressive tightening cycle to combat inflation. While inflation has shown signs of cooling, the “last mile” of bringing it down to the 2% target is often the most difficult.

The Transmission Mechanism

How do central bank rates affect your mortgage?

Policy Rate: The BoC sets the overnight rate.

Prime Rate: Commercial banks adjust their prime rate in lockstep.

Variable Mortgages: Directly tied to prime, payments increase immediately.

Fixed Mortgages: Tied to bond yields (specifically the 5-year Government of Canada bond). Bond yields are influenced by inflation expectations and BoC policy.

The “Higher for Longer” Narrative

In 2023, the market hoped for rapid rate cuts in 2024. However, sticky inflation in the services sector has forced the BoC to maintain a “higher for longer” stance. If rates remain elevated through 2025, the cumulative stress on household balance sheets will peak in 2026.

Inflation’s Dual Role

Inflation impacts the housing market in two contradictory ways:

Negative: It forces interest rates up, making mortgages expensive (Demand destruction).

Positive: It increases the replacement cost of homes (construction materials, labor), which can put a floor under housing prices (Supply cost).

In the context of the housing market recession 2026, the demand destruction aspect is currently outweighing the supply cost aspect. Buyers simply cannot qualify for loans large enough to meet the asking prices dictated by construction costs.

Debt-to-Income Ratios

Canadian household debt-to-income ratios are among the highest in the G7. When interest rates were near zero, this debt was manageable. As rates normalize, the service cost of that debt skyrockets.

Scenario A (Soft Landing): Inflation drops, rates fall to 3%, economy grows slowly. Housing stagnates.

Scenario B (Hard Landing/Recession): Inflation spikes again, rates stay high, unemployment rises. This is the scenario leading to the housing market recession 2026.

4.Historical Context: Comparing 2026 to Past Housing Corrections

To predict the future, we must analyze the past. Canada has experienced housing corrections before. Understanding the differences between those periods and the projected 2026 scenario is crucial for risk assessment.

The Early 1990s Recession

In the early 90s, Canada faced a severe recession combined with a housing crash.

Cause: Sky-high interest rates (double digits) to kill inflation.

Outcome: Prices dropped significantly (20-30% in some areas), and it took nearly a decade to recover.

Comparison to 2026: Interest rates today are high, but not at 1990 levels (14%). However, household debt loads are significantly higher now than in 1990. This makes the modern consumer more vulnerable to rate shocks, even if the rates themselves are lower.

The 2008 Global Financial Crisis

Interestingly, Canada largely sidestepped the 2008 housing crash that devastated the US.

Reason: Stricter banking regulations and a lack of subprime lending.

Outcome: A brief pause in price growth, followed by a massive bull run fueled by low rates.

Comparison to 2026: The regulatory framework is even stricter now (stress tests, B-20 guidelines). This prevents a US-style foreclosure crisis but contributes to the “subdued demand” by locking buyers out. The housing market recession 2026 is likely to be a volume recession (low sales) rather than a foreclosure crisis.

The 2017-2018 Cool Down

Foreign buyer taxes and mortgage rule changes in Ontario and British Columbia caused a temporary dip.

Outcome: Prices flattened or dipped slightly, then resumed climbing by 2019.

Comparison to 2026: The 2017 cool-down was policy-driven. The 2026 projection is fundamentals-driven (affordability and rates). Policy-driven dips are often bought by investors. Fundamentals-driven dips are harder to trade because the math doesn’t work for cash flow.

Table 2: Historical Housing Corrections vs. 2026 Forecast

| Feature | Early 1990s | 2008 Crisis | 2017 Cool Down | 2026 Forecast (CMHC) |

| **Primary Trigger** | Interest Rates | Global Credit Crunch | Government Policy | Affordability & Rates |

| **Price Decline** | Severe (-20%+) | Minimal | Moderate (-5 to -10%) | Moderate to Severe (Regional) |

| **Duration** | 5+ Years | < 1 Year | 18 Months | 24-36 Months |

| **Unemployment** | High | Moderate | Low | Rising |

| **Mortgage Rates** | > 10% | ~5% | ~3% | ~4-5% |

| **Household Debt** | Low | Moderate | High | Very High |

This comparison highlights that while the housing market recession 2026 may not see double-digit interest rates, the vulnerability of the consumer is at an all-time high.

5.5. Regional Analysis: Who Will Be Hit Hardest?

Canada is not a monolith. A national average often hides extreme regional variances. The housing market recession 2026 will not affect every province equally.

Toronto and the Greater Golden Horseshoe (GTA)

Toronto has been the engine of Canadian real estate growth. However, it is also the most unaffordable.

Risk Level: High.

Vancouver has historically been insulated by foreign capital and geographic constraints.

Risk Level: Moderate-High.

Why: Foreign buyer bans have reduced one pillar of demand. However, limited land supply supports long-term values.

Prediction: Detached homes in prime areas will hold value; suburban and condo markets may soften significantly.

Montreal, Quebec

Montreal has been the “affordable” alternative for years, leading to a surge in migration from Ontario.

Risk Level: Moderate.

Why: Prices rose rapidly recently, catching up to national averages. Affordability is eroding fast.

Prediction: A pause in growth rather than a sharp crash. The cultural preference for stability may buffer the market.

Calgary and Alberta

Alberta has seen a resurgence due to interprovincial migration and energy sector stability.

Risk Level: Low-Moderate.

Why: Still more affordable than Ontario/BC. Strong job market in energy.

Prediction: Continued resilience. Alberta may be the outlier that avoids the housing market recession 2026 severity seen elsewhere.

Atlantic Canada (Halifax, etc.)

The pandemic boom saw massive price spikes in the Maritimes.

Risk Level: High.

Why: Prices doubled in some areas without corresponding wage growth. Remote work trends are normalizing, reducing the “work from anywhere” premium.

Prediction: Significant correction possible as remote workers return to hubs or affordability caps out.

Table 3: Regional Vulnerability Index

| Region | Affordability Score | Employment Stability | Supply Pipeline | Recession Risk (2026) |

| **Toronto (GTA)** | Very Low | High | High (Condos) | **High** |

| **Vancouver** | Very Low | Moderate | Low | **High** |

| **Montreal** | Moderate | Moderate | Moderate | **Medium** |

| **Calgary** | Moderate | High | Moderate | **Low** |

| **Ottawa** | Low | High (Govt) | Low | **Medium** |

| **Halifax** | Low | Moderate | Low | **High** |

6.The Supply Side: Construction Slowdowns and Zoning

While demand is subdued, what is happening on the supply side? Conventional economic theory suggests that if demand drops, prices drop. However, if supply drops faster than demand, prices can remain stable or even rise.

The Construction Slowdown

High interest rates affect developers too. Construction loans are expensive. If developers cannot pre-sell units because buyers cannot get mortgages, projects get cancelled.

CMHC Data: There has been a noticeable increase in project cancellations in high-density urban centers.

Impact: This reduces the future supply of homes. By 2026, the lack of new inventory could act as a floor for prices, preventing a total collapse.

Zoning and Red Tape

Municipal zoning laws remain a significant bottleneck. While the Federal government is pushing for densification (allowing multiplexes in single-family zones), municipal implementation is slow.

NIMBYism: “Not In My Backyard” sentiment continues to delay approvals.

Development Charges: Cities have increased development charges to fund infrastructure, passing costs to buyers.

The “Missing Middle”

Canada faces a skilled labor shortage in the trades. An aging workforce of electricians, plumbers, and carpenters means construction costs remain sticky. Even in a recession, building a home remains expensive, which supports the resale value of existing stock.

7.Demographic Shifts: Immigration and Population Growth

One of the strongest arguments against a severe housing market recession 2026 is Canada’s demographic trajectory.

Record Immigration Levels

Canada has one of the highest per-capita immigration rates in the world. The federal government has set targets to welcome over 500,000 new permanent residents annually.

Demand Driver: Every new resident needs a place to live. This creates fundamental demand that is independent of interest rates.

The Counter-Argument: While immigration drives housing demand (rentals and purchases), it does not necessarily drive mortgage-qualified demand. New immigrants often rent initially. If the rental market becomes saturated, this could indirectly impact the purchase market.

Population Growth vs. Housing Starts

For the past three years, population growth has significantly outpaced housing starts.

The Gap: This deficit creates a structural shortage.

2026 Outlook: If immigration targets are maintained, the sheer volume of people could absorb the excess inventory caused by the recession. This suggests the housing market recession 2026 might be a “price recession” (stagnation) rather than a “vacancy recession” (empty homes).

The Aging Population

Conversely, Canada has an aging population. Baby Boomers hold a significant portion of the housing wealth.

Downsizing Trend: As Boomers age, some will downsize, releasing stock to the market.

Inheritance: However, many intend to pass homes to children.

Impact: A surge in downsizing in 2026 could add supply pressure, exacerbating the subdued demand issue.

- The Mortgage Renewal Wall: A Ticking Time Bomb?

This is perhaps the most critical technical factor contributing to the housing market recession 2026.

The 5-Year Cycle

Most Canadian mortgages are fixed for 5 years.

2020-2021: Homeowners locked in rates between 1.5% and 2.5%.

2025-2026: These mortgages come up for renewal.

The Shock: Renewing at 4.5% or 5% represents a payment increase of 30% to 50% for some households.

Forced Sales

When payments become unmanageable, homeowners have three choices:

Pay the difference: Dip into savings (which are depleted).

Extend amortization: Lengthen the mortgage to 30 or 35 years (increases total interest).

Sell the home: This adds supply to the market.

If a wave of forced sales hits the market in 2025 and 2026 simultaneously with subdued buyer demand, prices will correct. This is the mechanism by which the renewal wall fuels the housing market recession 2026.

HELOCs and Second Mortgages

Many homeowners used Home Equity Lines of Credit (HELOCs) during the pandemic to finance renovations or consumption. These are often variable rate. Payments on these have already increased. This reduces the disposable income available to service the primary mortgage renewal.

- Impact on Stakeholders: Buyers, Sellers, and Investors

How does the housing market recession 2026 affect different players in the ecosystem?

For the First-Time Buyer

The Good: Less competition. Bidding wars may vanish. Conditions (inspections, financing) may become acceptable again.

The Bad: Banks may tighten lending criteria. Appraisals might come in lower than offer prices.

Strategy: Focus on stability of employment over speculation. Get pre-approved but understand rates can change.

For the Current Homeowner (Seller)

The Good: If you have a low rate, you are in a strong position relative to new buyers.

The Bad: If you need to sell to buy up, you face the same market conditions on both sides. Equity may erode.

Strategy: Price realistically. Overpriced homes will sit indefinitely in a subdued market.

For the Real Estate Investor

The Risk: Negative cash flow. If rents do not cover the new mortgage payments + maintenance + taxes, the asset becomes a liability.

The Opportunity: Distressed sales. Investors with cash reserves can purchase properties below market value from forced sellers.

Strategy: Run conservative pro formas. Assume vacancy rates of 5% and maintenance costs of 1% of value annually. Do not rely on appreciation to justify the purchase.

For the Renter

The Paradox: A housing recession does not guarantee lower rents. If investors sell rental units to owner-occupiers, rental supply shrinks, potentially driving rents up even if sale prices drop.

Outlook: Rents are expected to remain high due to the fundamental shortage of rental units.

- Government Policy: Interventions and Regulatory Changes

Governments rarely sit idle during a housing crisis. We can expect policy interventions leading up to and during the housing market recession 2026.

Potential Federal Interventions

First Home Savings Account (FHSA): Already implemented, but limits may be increased to stimulate demand.

Mortgage Stress Test: The government could relax the stress test requirements to help buyers qualify. Risk: This could reignite inflation.

Immigration Targets: A reduction in temporary resident caps could ease rental pressure.

Provincial Interventions

Land Transfer Taxes: Temporary rebates or reductions to encourage activity.

Zoning Reform: Mandating density near transit hubs to speed up supply.

Rent Controls: Tightening rules on evictions and rent increases to protect tenants during economic hardship.

The Political Cycle

2025 is a federal election year in Canada. Housing is a top voter concern. Governments may introduce populist measures to stabilize prices before the election, which could artificially prop up the market heading into 2026.

- Investment Strategies for a Cooling Market

If the housing market recession 2026 materializes, traditional “buy and hold” strategies may need adjustment.

Cash is King

In a high-interest environment, liquidity provides optionality. Investors with cash can negotiate significant discounts.

Strategy: Maintain higher cash reserves. Avoid being fully leveraged.

Focus on Cash Flow

Speculative buying (buying for appreciation only) is dangerous in a recession.

Strategy: Buy properties that generate positive cash flow from Day 1, even at current interest rates. This usually means looking outside major city centers or buying multi-unit properties.

Diversification

Do not put all capital into one market.

Strategy: Consider diversifying into REITs (Real Estate Investment Trusts) which offer liquidity, or exploring different geographic markets (e.g., investing in Alberta while Ontario cools).

The “Barbell” Approach

Safe End: Pay down existing debt to reduce exposure to renewal shocks.

Aggressive End: Keep dry powder ready to acquire distressed assets if the market crashes harder than expected.

- The Rental Market Paradox

It is essential to distinguish between the ownership market and the rental market. The CMHC warning focuses on housing starts and sales. However, the rental market operates on different fundamentals.

Supply Shortage

Canada has a chronic shortage of purpose-built rental apartments.

Impact: Even if condo prices drop, rents may not. Landlords will pass on higher mortgage costs to tenants where possible.

Vacancy Rates: National vacancy rates remain historically low (below 2% in major cities).

The Investor Exit

If the housing market recession 2026 causes small-scale investors to sell, who buys the properties?

Scenario: If they are sold to owner-occupiers, rental supply drops -> Rents Rise.

Scenario: If they are sold to other investors, rental supply stays stable -> Rents Stabilize.

Most Likely: A mix, but overall rental affordability will remain a crisis independent of the resale market recession.

Table 4: Ownership Market vs. Rental Market Outlook 2026

| Feature | Ownership Market | Rental Market |

| **Price Trend** | Downward / Stagnant | Upward / Stable |

| **Demand Driver** | Mortgage Qualification | Need for Shelter |

| **Supply Constraint** | High Interest Rates | Construction Lag |

| **Volatility** | High | Low |

| **Investor Sentiment** | Cautious / Bearish | Bullish (for Yield) |

- Long-Term Outlook: Recovery Beyond 2026

Is the housing market recession 2026 the end of the road for Canadian real estate? Unlikely. Real estate is cyclical.

The Recovery Phase

Historically, after a correction, the market enters a consolidation phase followed by recovery.

Timeline: If the recession hits in 2026, recovery might begin in 2027 or 2028.

Catalyst: Interest rate cuts. Once the Bank of Canada begins cutting rates aggressively to stimulate the broader economy, borrowing costs will fall, reigniting demand.

The New Normal

The market post-2026 will likely look different than the market pre-2020.

Lower Leverage: Buyers will be more cautious about debt.

Smaller Homes: The average square footage per person may decrease.

Suburban Shift: Remote work may stabilize, but the desire for space remains.

Wealth Implications

For those who hold through the downturn, long-term wealth generation remains possible. Real estate has historically outpaced inflation over 20-year horizons. The housing market recession 2026 should be viewed as a cycle within a longer secular trend of urbanization and population growth.

- Conclusion

The warning from the CMHC regarding a potential housing market recession 2026 is a sobering reminder that no market goes up forever. The convergence of high interest rates, elevated household debt, and affordability constraints has created a fragile environment. “Subdued demand” is the euphemism for a market that has priced out its own participants.

However, panic is not a strategy. While the risks are real, Canada’s strong immigration targets and chronic supply shortages provide a safety net that may prevent a catastrophic collapse. The most likely outcome is a period of stagnation and correction, particularly in overvalued segments like urban condos, while essential housing in affordable regions remains resilient.

For stakeholders, the path forward requires diligence. Buyers should prioritize affordability over speculation. Sellers must price realistically. Investors need to focus on cash flow. And policymakers must balance the need to cool prices with the necessity of building homes.

The housing market recession 2026 is not a certainty, but it is a probability that demands preparation. By understanding the data, the regional nuances, and the economic levers at play, Canadians can navigate this upcoming cycle with their financial health intact. The era of easy money is over; the era of strategic real estate management has begun.

Frequently Asked Questions About the 2026 Housing Market

What does the CMHC predict for the housing market in 2026?

The CMHC (Canada Mortgage and Housing Corporation) has indicated a risk of a housing market recession in 2026. Their forecast suggests “subdued demand” due to high interest rates, affordability issues, and economic uncertainty. They project a potential decline in housing starts and resale activity, with price corrections in overvalued regions.

Will home prices crash in Canada in 2026?

While a “crash” implies a sudden, catastrophic drop, the CMHC forecast points more toward a correction or stagnation. Prices may decline in high-risk areas like Toronto and Vancouver condos, but strong population growth and supply shortages may prevent a nationwide collapse. Regional variance is expected to be high.

How will interest rates affect the 2026 housing market?

Interest rates are the primary driver of the potential recession. Many homeowners face mortgage renewals between 2025 and 2026 at much higher rates than their original terms. This reduces disposable income and may force some sales, increasing supply while high rates simultaneously reduce buyer demand.

Is now a good time to buy a home before the 2026 recession?

Timing the market is difficult. If you can afford the payments at current stress-test rates and plan to hold the property for 10+ years, buying may still be viable. However, buyers should be cautious about over-leveraging and ensure they have a buffer for potential price fluctuations or income changes.

How does immigration impact the housing recession forecast?

Canada’s high immigration targets create fundamental demand for housing. This acts as a counterbalance to the recessionary pressures. While mortgage-qualified demand may be subdued, rental demand is expected to remain strong, which could support investment properties even if resale prices soften.

What should investors do to prepare for a housing market recession?

Investors should focus on cash-flowing properties rather than speculative appreciation. Maintaining cash reserves, reducing debt leverage, and diversifying portfolios are key strategies. It is also advisable to review mortgage terms and prepare for potential vacancy periods.